No Loss Offset Rule in India: Impact on Crypto Traders

Imagine you make a profit of ₹100,000 on one Bitcoin trade but lose ₹80,000 on another Ethereum trade. Your net result is a modest gain of ₹20,000. In most traditional investment scenarios, you would pay tax only on that ₹20,000. But if you are a crypto trader operating under India's current regulatory framework, the reality is much harsher. You owe 30% tax on the full ₹100,000 gain-₹30,000-while your ₹80,000 loss provides zero relief. This asymmetry is not a bug; it is the core feature of the no loss offset rule codified under Section 115BBH(2)(b) of the Income Tax Act.

This rule fundamentally changes how Indian investors approach digital assets. It transforms cryptocurrency from a standard investment vehicle into a high-risk tax liability trap for many active traders. As we move through 2026, understanding this specific restriction is critical for anyone holding or trading Virtual Digital Assets (VDAs) in India.

Understanding the No Loss Offset Rule

The no loss offset rule is a specific provision within India’s crypto tax regime that prohibits traders from using losses incurred on one crypto transaction to reduce the taxable gains from another. Unlike equity markets or business income, where losses can often be set off against profits to determine the true net income, crypto losses are effectively ignored by the taxman when calculating your liability on gains.

Here is how it works in practice:

- No Set-off Within Crypto: If you sell Bitcoin at a profit and Ethereum at a loss, you cannot subtract the ETH loss from the BTC profit. You pay 30% tax on the gross BTC profit alone.

- No Carry Forward: Unused losses cannot be carried forward to future financial years. Once the year ends, those losses vanish for tax purposes.

- No Cross-Asset Offsetting: You cannot use crypto losses to offset gains from stocks, mutual funds, or salary income. The silo is complete.

This creates what tax experts call an "asymmetric tax burden." You are taxed on every winning trade individually, but penalized with no credit for losing trades. For a trader who wins small often but loses big occasionally, this structure can result in paying significant taxes even when their overall portfolio is down for the year.

| Feature | Cryptocurrency (VDA) | Equity/Stocks |

|---|---|---|

| Tax Rate on Gains | Flat 30% | 10% (LTCG above ₹1.25L) / 15% (STCG) |

| Loss Offset Allowed? | No | Yes (within same category) |

| Carry Forward Losses? | No | Yes (up to 8 years) |

| Deductions for Expenses | Only acquisition cost | Brokerage, STT, etc. |

The Broader Tax Framework: 30% + TDS

To fully grasp the impact of the no loss offset rule, you must look at the entire ecosystem of India's crypto taxation introduced in 2022 and tightened in subsequent budgets. The rule does not exist in isolation; it works alongside other restrictive measures.

The Flat 30% Tax Rate All gains from Virtual Digital Assets are taxed at a flat 30%, plus applicable surcharge and cess. This rate applies regardless of your income slab. Whether you earn ₹5 lakh or ₹5 crore annually, your crypto gains are taxed at the same percentage. There is no distinction between short-term and long-term capital gains for crypto, unlike equities where holding periods matter.

1% Tax Deducted at Source (TDS) Under Section 194S, exchanges must deduct 1% TDS on the total value of crypto transfers exceeding ₹10,000 per year (₹50,000 for certain entities). This happens at the time of transaction. While TDS is adjustable against your final tax liability, it creates immediate cash flow issues. You lose liquidity on every trade, which is particularly painful for active traders who need capital to reinvest.

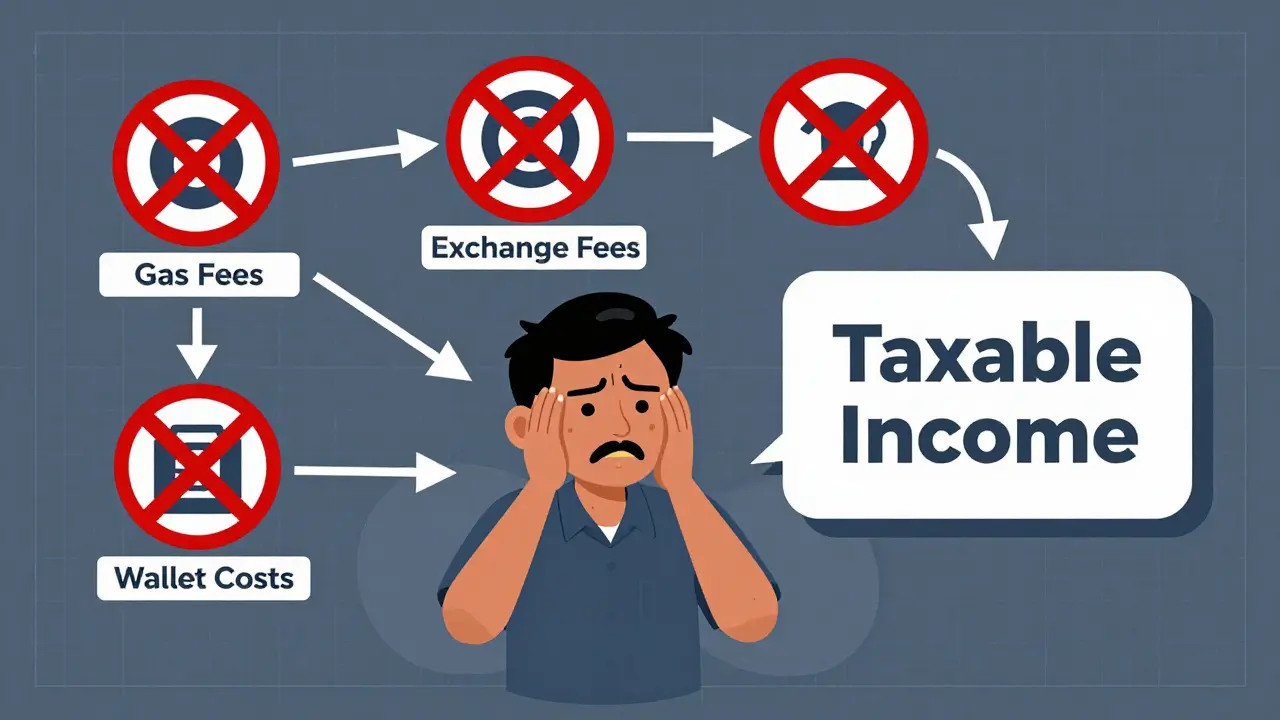

Limited Deductions The law allows you to deduct only the cost of acquisition. You cannot claim operational expenses such as gas fees (network transaction costs), exchange listing fees, or wallet storage costs. This means your taxable base is higher than your actual economic gain.

Real-World Impact on Trader Psychology and Strategy

The combination of these rules has drastically altered behavior among Indian crypto participants. Platforms like CoinSwitch have reported that regulations are "stricter than ever," warning that non-compliance carries severe risks. But compliance itself is becoming a deterrent.

Reduced Trading Volume Many retail traders have shifted from active day-trading to long-term holding ("HODLing"). Why? Because frequent trading generates more taxable events without the ability to offset losses. A swing trader who makes five profitable trades and two large losing trades in a month pays tax on all five profits immediately. The psychological toll of paying tax on money you haven't actually kept (due to losses) is significant.

Migration to Derivatives A growing number of sophisticated traders are moving to crypto futures. Futures contracts are derivatives and do not fall under the definition of Virtual Digital Assets (VDA) in the same way spot holdings do. Consequently, they are not subject to the 1% TDS on transfer. However, this strategy carries its own risks, including higher leverage danger and potential future regulatory scrutiny.

Offshore Platform Usage Some users are turning to international exchanges to avoid domestic TDS mechanisms. However, this path is fraught with danger. Using the Liberalised Remittance Scheme (LRS) to send money abroad incurs a 20% Tax Collected at Source (TCS) on amounts exceeding ₹7 lakh. Furthermore, the government is increasingly cracking down on undisclosed foreign holdings.

Compliance Challenges and Reporting Burdens

Navigating the ITR filing process for crypto is complex. You cannot file the simple ITR-1 form if you have crypto gains. You must use ITR-2 or ITR-3, which require detailed disclosure in Schedule VDA.

Traders must maintain meticulous records of:

- Acquisition date and cost for every asset.

- Transfer date and value for every sale or swap.

- TDS certificates provided by exchanges.

For someone who trades frequently across multiple coins, manually tracking this data is nearly impossible. This has led to a surge in demand for specialized crypto tax software and advisory services. Firms like Dinesh Aarjav & Associates note that documentation is "non-negotiable." Failure to report accurately can lead to penalties, interest, and even prosecution for willful evasion.

Additionally, new complexities arise with staking rewards, airdrops, and hard forks. Staking rewards are taxed as "Income from Other Sources" when received, based on fair market value. When you later sell those staked tokens, you face capital gains tax again. This double taxation layer further complicates the ledger.

Regulatory Outlook: 2025-2026 Developments

As of mid-2026, there is little sign of relief. The Budget 2025 introduced additional penalties for undisclosed VDA holdings. Authorities are now empowered to tax unreported crypto at a steep 60% rate under Section 158B, applicable retrospectively from February 1, 2025. This indicates an intensification of enforcement rather than a relaxation of rules.

Tax experts predict that the no loss offset rule will remain a permanent feature. Industry associations continue to advocate for reform, arguing that the current framework stifles innovation and drives activity underground. However, the government’s stance remains firm: crypto is treated as a speculative asset with high risk, warranting strict taxation.

The global context highlights India’s outlier status. Countries like the United States allow crypto losses to offset gains, and Germany offers tax-free gains after one-year holding periods. India’s approach is among the most restrictive globally, creating a unique challenge for local traders.

Strategies for Mitigation (Within Legal Bounds)

While you cannot change the law, you can optimize your approach. Here are practical steps:

- Consolidate Trades: Avoid unnecessary swaps. Each swap is a taxable event. Holding longer reduces the frequency of taxable events.

- Track Everything: Use automated tools to track acquisition costs and transaction histories. Accurate records prevent overpayment and ensure compliance.

- Understand TDS Adjustments: Ensure your exchange provides correct TDS certificates. Claim these adjustments during ITR filing to avoid paying tax twice.

- Consult Specialists: General CA advice may not suffice. Seek advisors familiar with VDA schedules and recent case laws.

Remember, attempting to evade taxes through offshore accounts without proper LRS reporting is risky. The penalty structure (60% tax on undisclosed income) far outweighs the savings from avoiding the 30% rate.

Can I offset crypto losses against stock market gains in India?

No. Under Section 115BBH, losses from Virtual Digital Assets cannot be set off against gains from any other source, including equity shares, mutual funds, or salary. The silo is strict.

What happens to my crypto losses if I don't make any gains in a year?

They are lost forever. India's crypto tax law does not allow carrying forward losses to future financial years. Unlike business losses which can be carried forward for eight years, crypto losses expire at the end of the assessment year.

Is the 1% TDS refundable?

Yes, but only against your final tax liability. If the TDS deducted exceeds your total tax payable for the year, you can claim a refund during ITR filing. However, the cash is blocked until you file your returns.

Do I pay tax on swapping Bitcoin for Ethereum?

Yes. Swapping one crypto for another is treated as a sale of the first asset and purchase of the second. You must calculate capital gains based on the fair market value of the Bitcoin sold at the time of swap. This triggers both tax liability and potential TDS.

Are gas fees deductible from my crypto gains?

No. The law explicitly limits deductions to the cost of acquisition only. Operational expenses like network gas fees, exchange withdrawal fees, or wallet storage costs cannot be claimed as deductions against your gains.