Multi-Jurisdictional Compliance in Blockchain: Navigating Global Legal Risks

When you run a blockchain project that serves users in Europe, Asia, and the U.S., you're not just dealing with code. You're tangled in a web of laws that change every week. One country says you must delete user data. Another demands you store it for seven years. A third bans anonymous wallets entirely. This isn't theory - it's daily reality for any blockchain team operating across borders. Multi-jurisdictional compliance isn't optional. It's the difference between scaling globally and getting shut down overnight.

Why Blockchain Makes Compliance Harder

Blockchain was built to be borderless. Transactions happen instantly between strangers in Tokyo, Lagos, and Toronto. But laws don’t move that fast. Each country has its own rules about who can use your platform, what data you must collect, and how you handle user privacy. And they don’t talk to each other. Take GDPR in the European Union. It says users can demand their data be erased. But in China, regulators require you to keep transaction records for five years. In the U.S., states like California (CCPA) and Virginia (VCDPA) have their own privacy laws that overlap and conflict. If your blockchain wallet collects an email, IP address, or even a wallet ID - you’re processing personal data under GDPR. That means you must comply even if your company is based in New Zealand. And it gets worse. Some jurisdictions treat crypto assets as property. Others treat them as currency. A few classify them as securities. Your smart contract that works fine in Singapore might be illegal in Brazil because it resembles an unregistered investment product.The Real Cost of Getting It Wrong

Fines aren’t just numbers. They’re existential. Under GDPR, companies can be fined up to 4% of their global revenue. For a startup with $50 million in annual turnover, that’s $2 million - gone in one violation. But the bigger threat isn’t the fine. It’s the loss of trust. Wells Fargo lost $3 billion and its reputation because employees created fake accounts across states. A blockchain project can face the same fate. Imagine your DeFi app is used by 100,000 EU users. One day, a regulator in Germany finds that your KYC process doesn’t meet local identity verification rules. You’re ordered to freeze all EU accounts. Your user base collapses. Investors pull out. Your token price crashes. All because you assumed your U.S.-based compliance policy covered the world. In 2023, Regology recorded over 700,000 regulatory changes in the U.S. alone. That’s more than 1,900 new rules or updates every single day. Blockchain projects don’t get exemptions. If your platform touches a user in France, Canada, or Australia, you’re subject to their rules - whether you intended to or not.

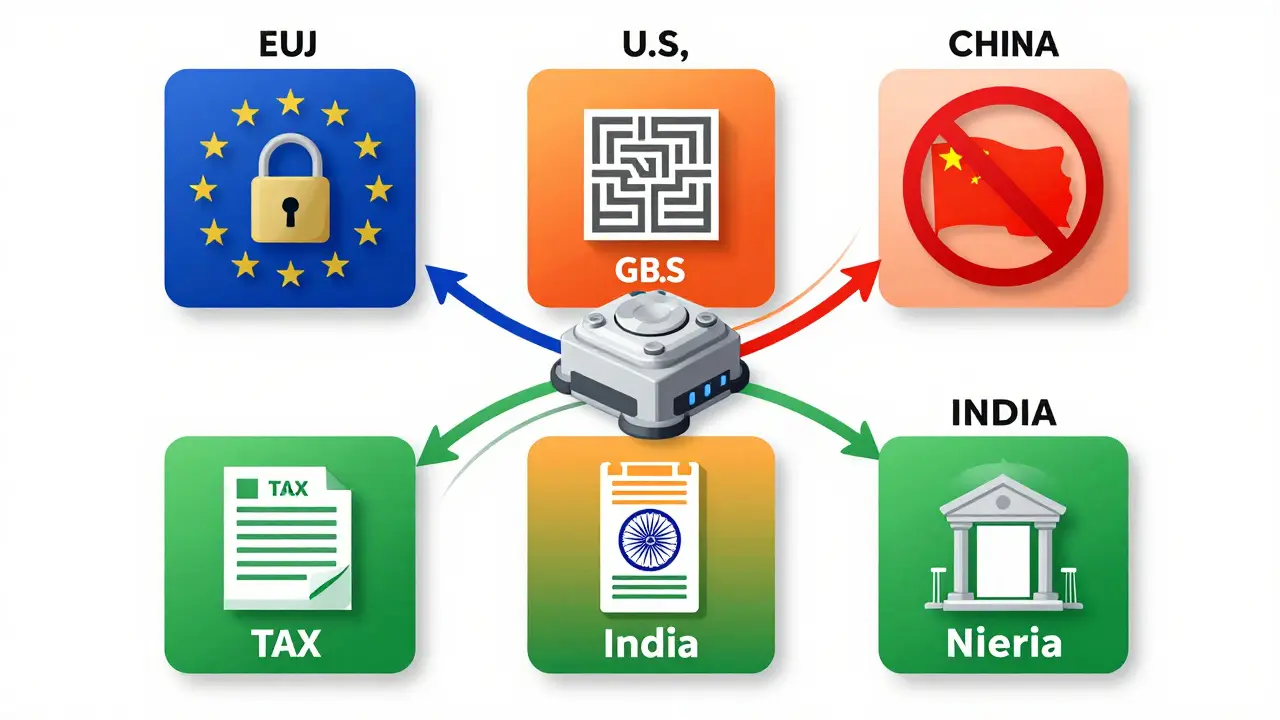

Five Jurisdictions That Will Break Your Compliance

Not all regions are equal. Some are predictable. Others are minefields.- European Union (GDPR + MiCA): GDPR applies to any company handling EU citizen data - even if you’re based in Singapore. MiCA (Markets in Crypto-Assets), effective in 2024, adds licensing rules for crypto service providers. You need a legal entity in the EU to operate legally.

- United States: No federal crypto law. Instead, you juggle the SEC (securities), FinCEN (money transmission), state-level money transmitter licenses (50+ states), and privacy laws like CCPA. A single app can need 10+ registrations.

- China: Crypto trading is banned. Mining is illegal. Even offering blockchain education can trigger scrutiny. If your platform has any Chinese user, you risk being blocked or fined under national cybersecurity laws.

- India: Crypto is legal but taxed at 30% with no deductions. You must report all transactions to tax authorities. Failure to report can lead to criminal charges under the Income Tax Act.

- Nigeria: The Central Bank banned banks from serving crypto firms in 2021. Though lifted in 2023, enforcement remains inconsistent. You could be shut down tomorrow based on a local regulator’s interpretation.

Running a global blockchain service without mapping these five alone is like driving blindfolded through a minefield.

What You Must Track

You can’t comply if you don’t know what you’re complying with. Here’s what every blockchain team needs to monitor:- Data handling rules: Where is user data stored? Who can access it? Can users delete it? Can you transfer it across borders?

- Know Your Customer (KYC): Some countries require ID verification. Others forbid collecting government IDs. Some require biometrics. Others ban facial recognition.

- Tax obligations: Are you selling a service? A financial product? A commodity? Each has different tax rules. Are you collecting VAT? Sales tax? Withholding tax?

- Consumer protection laws: Can users reverse transactions? Do you need a dispute resolution process? Are you liable for smart contract bugs?

- Advertising rules: Can you say "earn 15% APY"? Can you use influencers? Are you required to disclose risks in a specific font size?

One team we worked with in Wellington assumed their U.S. privacy policy covered global users. Then they got a letter from Spain’s data protection authority: they were violating GDPR because they stored EU users’ wallet addresses on U.S.-based servers without a data transfer agreement. They had to rebuild their entire data flow in three weeks.

Solutions That Actually Work

There’s no magic bullet. But there are proven strategies.- Build regional zones: Don’t run one global app. Create separate instances for EU, U.S., Asia, etc. Each has its own compliance layer. This isn’t ideal - but it’s safer than trying to merge everything.

- Use AI-powered compliance tools: Platforms like Athennian and Regology track regulatory changes in real time. They don’t just alert you - they tell you what to change. A blockchain team using one of these tools reduced compliance errors by 70% in six months.

- Partner with local legal firms: Don’t rely on your in-house counsel. Hire a lawyer in each major jurisdiction you serve. Pay them a monthly retainer to review updates. It’s cheaper than a $10 million fine.

- Document everything: Keep a centralized register of every law you’re subject to. Note the jurisdiction, the requirement, the date it changed, and who’s responsible for compliance. If you get audited, this is your shield.

One startup in Wellington started by serving only New Zealand. They added Australia next. Then the U.S. Then the EU. Each time, they paused development to map the legal risks. It slowed them down - but they never got a single regulatory notice. Their competitors? Half are shut down.

The Future Is Worse

Regulators aren’t slowing down. They’re getting smarter. In 2025, the EU will start requiring blockchain projects to prove they can freeze illicit funds. The U.S. is pushing for mandatory reporting of cross-chain transactions. India wants real-time transaction monitoring. China is testing a digital yuan that could block access to non-compliant crypto platforms. The next five years will see more fragmentation, not less. The idea of a "global crypto standard" is dead. The winners won’t be the ones with the best tech. They’ll be the ones with the best legal infrastructure.If you’re building a blockchain product today and ignoring multi-jurisdictional compliance, you’re not innovating. You’re gambling.

Does GDPR apply to my blockchain project if I’m not in Europe?

Yes. GDPR applies to any organization that processes personal data of individuals in the EU - regardless of where the company is based. If your blockchain wallet collects an email, IP address, or even a public wallet ID from a user in France, Germany, or Spain, you’re subject to GDPR. You must allow data access requests, provide transparency about data use, and ensure secure storage. Failing to comply can result in fines up to 4% of your global revenue.

Can I use one compliance policy for all countries?

No. Every major jurisdiction has unique rules. A single employee handbook or privacy policy won’t cover you. California’s CCPA requires different disclosures than Germany’s BDSG. India’s tax rules don’t match Australia’s. Trying to use a one-size-fits-all approach is the most common reason blockchain projects get fined. You need localized policies - even if they’re built from a common framework.

What happens if I ignore compliance in one country?

You risk being blocked, fined, or sued. In 2023, a U.S.-based DeFi platform was ordered to shut down in Brazil after failing to register as a financial service provider. In the EU, a crypto exchange lost its license for not verifying user identities properly. Even if you’re small, regulators can target you. They don’t care if you’re a startup. They care if you’re operating illegally in their territory.

Do I need a legal entity in every country I serve?

Not always - but often. Some countries require you to have a local legal presence before you can offer services. For example, the EU’s MiCA regulation requires crypto firms to be incorporated within the bloc. In the U.S., you need a money transmitter license in each state where you have users. Skipping this step may seem like a shortcut, but it’s a legal time bomb. Your platform could be frozen without warning.

How often do blockchain regulations change?

Constantly. In 2023, the U.S. alone saw over 700,000 regulatory change events. Many jurisdictions update rules monthly. A new data privacy law can drop in Japan. A tax ruling can shift in Canada. A court decision can redefine what counts as a security in Australia. If you’re not monitoring changes daily, you’re already out of date. Automated compliance tools are no longer optional - they’re essential.

20 Comments

This whole thing is a mess. One day you're fine, next day some country bans your app. No warning. No grace period. Just boom. You're done.

Oh sweet, so now we're supposed to hire a lawyer for every country we have a single user in? Brilliant. Let me just take out a second mortgage on my sanity.

India taxes crypto at 30%? Bro. That's not regulation. That's extortion. And they still let people trade? LOL.

You're all missing the point. The real issue is the ontological mismatch between blockchain's decentralized architecture and state-centric regulatory frameworks. It's not about compliance-it's about epistemic hegemony.

Look, I get it's chaotic-but it’s not impossible. I’ve seen teams build regional zones, use AI tools, and hire local lawyers. It’s not sexy, but it works. You don’t need to be a giant to survive. Just be smart.

I just started my project in NZ and thought, 'eh, we'll figure it out later.' Now I'm terrified. But honestly? This post saved me. Thanks.

Oh, so now we’re supposed to obey 50 different governments… while pretending blockchain is 'decentralized'? That’s like saying a dog is a cat because it has four legs. The entire premise is a joke.

I’ve worked with teams in 8 countries. The ones who survive? They build slowly. One region. One law. One audit. No shortcuts. It’s boring. But it works.

this is sooo much stress 😭 i just wanna make a wallet and chill why does every country have to be a drama queen 🤦♀️

China bans crypto. India taxes it. EU demands data deletion. US has 50 different rules. So what’s the point? Just give up and go work at Walmart.

I used to think compliance was just paperwork. Then I saw what happened to a friend’s startup. They stored EU data on AWS in Virginia. Got a letter from Spain. Had to rebuild everything. Took three months. Lost half their team. It’s not a tech problem. It’s a life problem.

Let me ask you something. If you’re building something meant to be global, shouldn’t you expect global complexity? This isn’t a bug. It’s a feature of operating in the real world. The question isn’t 'how do we avoid this?' It’s 'how do we adapt?'

I tried using one policy for everywhere. Got hit with a fine in Germany. Then California. Then Canada. Now I have a spreadsheet with 27 tabs. Each one has a different version. My lawyer cries when I send it to him. Worth it.

I love how blockchain was supposed to break borders, but now we’re building digital walls just to stay legal. Kinda poetic, honestly. We’re not fighting governments-we’re fighting human nature.

If you’re building a blockchain product and you don’t live in the U.S., you’re wasting your time. America’s the only country with real innovation. The rest are just bureaucrats in suits.

I appreciate the depth here. This isn’t just a technical guide. It’s a survival manual. I’m sharing this with my team tomorrow.

You’re all overthinking it. Just use a VPN. Block EU IPs. Ignore India. Let them cry. We’re not here to be nice. We’re here to build. 🚀

i read this whole thing and im still confused like did they say china bans mining or just trading or both?? idk anymore 🤷♀️

I’m not scared of regulation. I’m scared of people who think they can wing it. This post? It’s the truth. Do the work. Build the zones. Hire the lawyers. Don’t be a hero. Be smart. 💪

I’ve been doing this for 5 years. The teams that win? They don’t try to be global overnight. They start local. Then expand. One law at a time. It’s slow. But it’s the only way that doesn’t end in tears. 🙌