How to Earn Passive Income with DeFi: A Practical Guide for 2026

You have cryptocurrency sitting in your wallet. It’s just... sitting there. While traditional bank accounts offer less than 1% interest, the world of Decentralized Finance (DeFi) is a financial ecosystem built on blockchain technology that allows users to earn returns on their assets without intermediaries like banks. Also known as open finance, it has grown from a niche experiment into a multi-billion dollar industry. As of early 2025, over $112 billion was locked in these protocols. That money wasn’t just parked; it was working. But how do you tap into this system without losing your shirt? The answer isn’t one-size-fits-all. It depends on how much risk you can stomach and how much time you want to spend managing your portfolio.

The Core Mechanisms of Earning Yield

To make money passively in DeFi, you need to understand where the yield comes from. Unlike a bank that pays you interest from its profits, DeFi yields come from three main sources: trading fees, protocol revenue, or new token emissions. Knowing which source backs your return is critical because it determines whether the income is sustainable or if it’s a temporary incentive that will vanish.

Liquidity Provision is the engine of many DeFi platforms. When you provide liquidity, you deposit two tokens (like ETH and USDC) into a pool on an automated market maker (AMM) such as Uniswap is the largest decentralized exchange protocol that uses liquidity pools instead of order books to facilitate trades.. Traders pay fees to swap tokens, and those fees are distributed to you. In Uniswap v3, fees range from 0.01% to 1.00% depending on the volatility of the pair. If you’re providing stablecoin pairs, the fees are lower, but the risk of impermanent loss is also minimal. This is often considered the most "real" form of yield because it’s backed by actual usage of the platform.

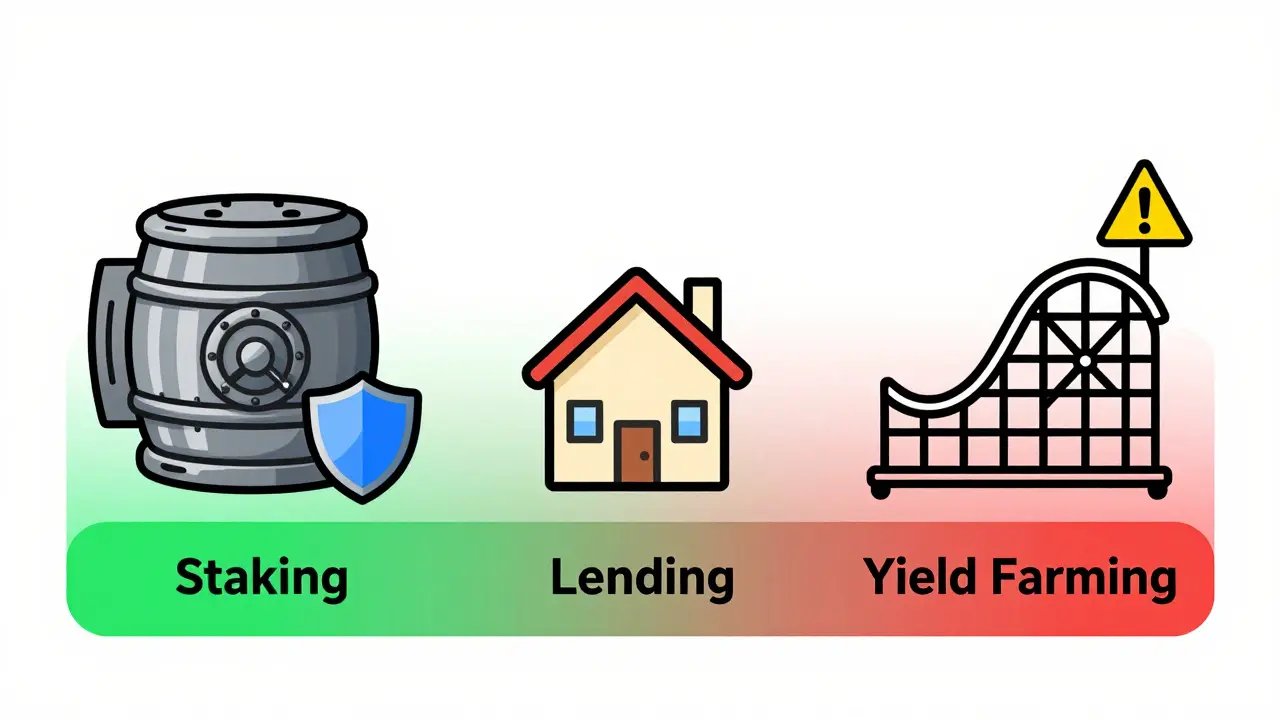

Staking involves locking up your tokens to secure a network. For Proof-of-Stake (PoS) blockchains like Ethereum, validators stake ETH to process transactions and earn rewards. You don’t need to run a validator node yourself. You can use delegated staking services like Lido is a liquid staking protocol that allows users to stake ETH without running their own nodes, receiving stETH in return.. As of Q1 2025, Lido managed over 12% of all staked ETH. The APY here typically ranges from 3% to 8%, depending on network demand. It’s relatively low-risk compared to other methods, but your capital is locked until you decide to unstake, which can take days during network congestion.

Lending protocols like Aave is a non-custodial liquidity protocol that enables users to supply assets to earn interest or borrow against them. and Compound work like digital banks. You deposit assets like USDC or DAI, and borrowers take them out, paying interest. The rate fluctuates based on supply and demand. In February 2025, USDC on Compound yielded around 4.8% APY. This is straightforward: you lend, they borrow, you get paid. The risk lies in the smart contract code-if there’s a bug, hackers can drain the pool.

Risk vs. Reward: Choosing Your Strategy

Not all DeFi income is created equal. Some strategies are easy but offer modest returns, while others promise high yields but carry significant danger. Here is a breakdown of the most common methods and their risk profiles.

| Strategy | Avg. APY (2025) | Difficulty | Primary Risk | Best For |

|---|---|---|---|---|

| Crypto Staking | 3-8% | Easy | Slashing, Lock-up periods | Long-term holders |

| Lending (USDC/DAI) | 4-10% | Medium | Smart contract bugs | Conservative earners |

| Liquidity Providing | Variable (2-50%) | Hard | Impermanent Loss | Active managers |

| Yield Farming | 10-100%+ (often unsustainable) | Very Hard | Token dilution, Rug pulls | High-risk speculators |

Yield Farming is where things get tricky. Protocols incentivize users to deposit assets by offering their own governance tokens as rewards. These advertised APYs can look insane-sometimes exceeding 50% or even 100%. However, these rewards are often printed out of thin air. If the value of the reward token drops faster than you earn it, you lose money. Data from Immunefi’s 2024 report showed that 68% of high-APY farming pools collapsed within 90 days. This is not passive income; it’s active speculation disguised as savings.

Dividend Tokens like KuCoin Token (KCS) offer another path. Holders receive a share of the exchange’s trading fees. KCS distributes about 50% of daily fee revenue to eligible holders. This is simple and requires no technical setup beyond holding the token. However, regulatory uncertainty looms large. The SEC’s aggressive stance on securities means tokens with dividend-like features face legal risks, as seen in the Ripple lawsuit.

Setting Up Your DeFi Infrastructure

Before you can earn, you need the right tools. The barrier to entry isn’t just financial; it’s technical. You’ll need a non-custodial wallet, gas fees, and a clear understanding of cross-chain bridges.

- Get a Wallet: Start with MetaMask is a popular browser extension and mobile app that acts as a gateway to interact with Ethereum-based dApps. or Trust Wallet. This gives you full control over your private keys. Never share these keys with anyone.

- Acquire Gas Tokens: You need ETH, MATIC, or BNB to pay for transaction fees. Even if you’re lending USDC on Polygon, you need MATIC to execute the transaction. Keep at least $50-$100 worth of native tokens handy.

- Use Bridges Carefully: To move assets between chains (e.g., from Ethereum to Arbitrum), you’ll use bridges like Hop or Stargate. These charge fees (usually 1-2%) and take time. Always verify the bridge’s security record before moving large sums.

- Verify Protocol Security: Only use protocols with multiple audits. Top-tier platforms like Aave and Uniswap have been audited by firms like OpenZeppelin and Trail of Bits. Check if they have insurance coverage through Nexus Mutual or InsurAce. As of Q1 2025, 67% of TVL was protected by some form of insurance.

Real-World Examples and Pitfalls

Let’s look at what actually happens when people try this. On Reddit’s r/DeFi community, a user shared their six-month journey in March 2025. They earned an 18.7% APY on stablecoins but suffered 12.3% impermanent loss due to ETH volatility. Their net return was only 6.4%. This highlights a crucial point: gross APY doesn’t equal net profit. You must account for impermanent loss, gas fees, and token depreciation.

On the flip side, success stories exist. A Bankless podcast featured a user generating $42,000 annually from a $500,000 portfolio diversified across 12 protocols. Their secret? Diversification and constant monitoring. They didn’t chase the highest APY; they chased sustainable yields between 4.8% and 7.2%.

Pitfalls are real. In January 2025, an oracle manipulation attack drained $3.8 million from Curve Finance’s sETH pool, affecting 1,200 users. This reminds us that even top protocols aren’t immune to hacks. Always keep a portion of your portfolio in cold storage or reputable centralized exchanges with insurance, like Coinbase, which offers 5.0% APY on USDC with FDIC-insured principal for institutional clients via JPMorgan’s Onyx division.

The Future of DeFi Income in 2026

As we move into 2026, the landscape is maturing. Ethereum’s Pectra hard fork in March 2025 reduced staking withdrawal times from days to hours, making staking more liquid. Institutional adoption is rising, with Grayscale’s DeFi Fund growing to $4.7 billion in assets under management. Regulatory clarity in the EU via MiCA provides a safer environment for European users, while the US remains volatile.

Experts predict that average stablecoin APYs will stabilize between 3.8% and 5.2% in 2026. The era of "easy money" with 50%+ APYs is fading. Instead, "real yield" protocols like Pendle Finance are gaining traction, where 87% of yields come from actual protocol revenue rather than token emissions. This shift favors long-term holders over short-term speculators.

If you’re new, start small. Use exchange-based staking for simplicity, then gradually move to direct protocol interaction as you gain confidence. Track your performance using dashboards like Dune Analytics. Remember, in DeFi, you are the bank. That means you bear the risk, but you also reap the rewards.

What is the safest way to earn passive income in DeFi?

The safest method is staking major cryptocurrencies like Ethereum or Solana through reputable, audited protocols. Another low-risk option is lending stablecoins like USDC on established platforms such as Aave or Compound. These methods offer moderate returns (3-8%) with lower volatility compared to yield farming.

Can I lose money earning passive income in DeFi?

Yes. Risks include smart contract bugs leading to hacks, impermanent loss in liquidity pools, and the collapse of the underlying asset. Additionally, if you’re earning rewards in a new token, its price could drop significantly, erasing your gains.

Do I need a lot of money to start?

No, you can start with as little as $50-$100. However, gas fees on networks like Ethereum can be high, so using Layer 2 solutions like Arbitrum or Polygon is recommended for smaller portfolios to maximize net returns.

What is impermanent loss?

Impermanent loss occurs when the price of deposited tokens changes compared to when you deposited them. If one token’s price rises or falls significantly relative to the other, you might end up with less value than if you had just held the tokens in your wallet. It becomes permanent if you withdraw during this state.

Is DeFi passive income taxable?

In most jurisdictions, yes. Interest, staking rewards, and liquidity mining earnings are typically treated as ordinary income. You should consult a tax professional familiar with cryptocurrency regulations in your country to ensure compliance.