How Indian Banks Handle Crypto-to-Fiat Withdrawals in 2026: A Guide to Restrictions and Compliance

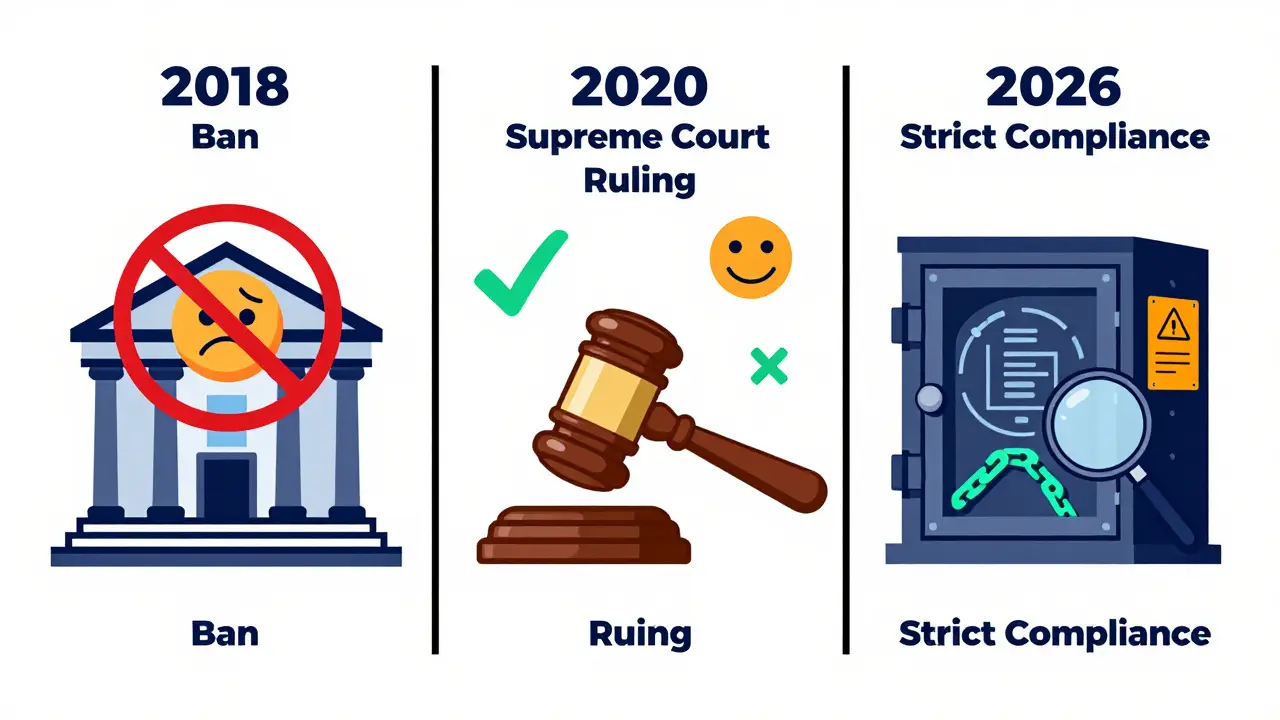

Withdrawing cryptocurrency for Indian Rupees (INR) used to be a nightmare. In 2018, the Reserve Bank of India (RBI) banned banks from processing any crypto-related transactions. But that changed in March 2020 when the Supreme Court struck down the ban. Today, you can legally buy, sell, and hold crypto in India. However, just because it is legal doesn’t mean your bank will happily process every transfer.

If you are trying to move funds from an exchange like CoinDCX, WazirX, or Binance to your bank account, you might still face friction. Banks are cautious. They operate under strict pressure from regulators to prevent money laundering and tax evasion. This guide explains exactly how Indian banks react to these withdrawals, what documentation you need, and why some transactions get flagged while others pass through smoothly.

The Current Legal Status of Crypto in India

To understand bank behavior, you first need to know the law. As of May 2026, owning cryptocurrency is not illegal in India. The landmark judgment by the Supreme Court in Internet and Mobile Association of India v Reserve Bank of India restored the right of exchanges to work with financial institutions. You can withdraw INR from a compliant exchange without fear of criminal prosecution simply for holding digital assets.

However, "legal" does not mean "unregulated." The government has tightened the screws significantly since 2023. Virtual Digital Asset (VDA) service providers-meaning crypto exchanges-are now fully regulated under the Prevention of Money Laundering Act (PMLA). This means exchanges must follow the same Know Your Customer (KYC) and Anti-Money Laundering (AML) rules as traditional banks. If an exchange fails to comply, the government shuts it down. We saw this happen in 2024-2025 when the Financial Intelligence Unit (FIU-IND) blocked access to over 25 offshore exchanges, including major platforms like BingX and LBank.

This regulatory environment creates a specific dynamic: banks are allowed to process crypto withdrawals, but they are terrified of getting fined if they process suspicious ones. Consequently, their reaction to your withdrawal depends heavily on whether the exchange you use is fully compliant with Indian laws.

Why Banks Flag Crypto Transactions

You might wonder why your bank suddenly asks for proof of income after years of smooth transfers. The answer lies in risk management. For a bank, a transfer labeled "Crypto Exchange" or originating from a known VDA provider triggers automated monitoring systems. Here is why they react negatively:

- Tax Evasion Concerns: The Indian government imposes a flat 30% tax on crypto profits and a 1% Tax Deducted at Source (TDS) on every sale. Banks want to ensure you aren't moving large sums without paying these taxes. If they suspect hidden income, they may freeze the transaction to report it to authorities.

- Money Laundering Risks: Cryptocurrencies are often used to obscure the origin of funds. Under the PMLA, banks are required to report any suspicious activity. A sudden influx of cash from a crypto source looks like classic layering-a technique used to clean dirty money.

- RBI Skepticism: Despite the Supreme Court ruling, the RBI remains deeply skeptical. Former Governor Shaktikanta Das and current Governor Sanjay Malhotra have repeatedly warned that crypto threatens financial stability. Banks listen to their regulator. When the central bank says "be careful," individual branch managers tend to err on the side of caution, sometimes blocking transactions even if they are technically legal.

This isn't personal. It's institutional self-preservation. Banks would rather lose a customer than pay a massive fine from the FIU-IND or the RBI.

Compliant vs. Non-Compliant Exchanges: The Key Difference

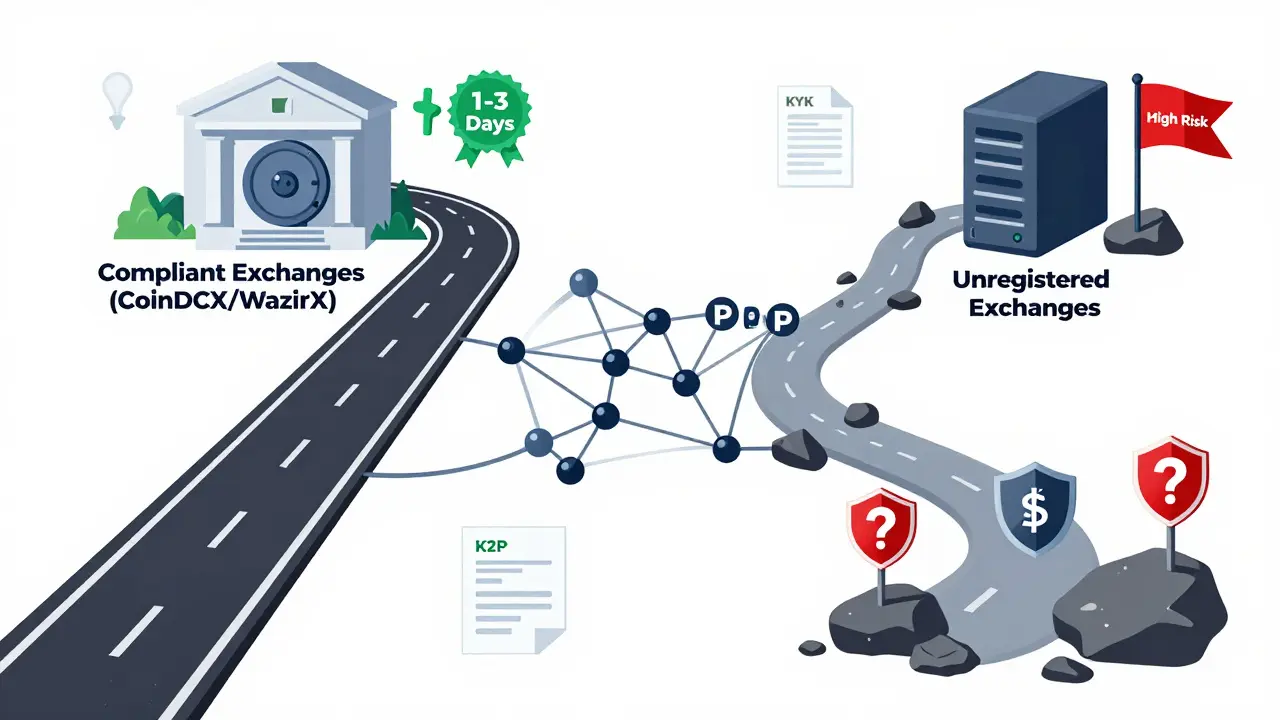

Your experience withdrawing fiat depends almost entirely on which platform you use. Not all exchanges are created equal in the eyes of Indian banks.

| Exchange Type | Regulatory Status | Bank Reaction | Withdrawal Speed |

|---|---|---|---|

| Fully Compliant (e.g., CoinDCX, WazirX) | Registered with FIU-IND, full KYC/AML integration | Generally smooth. Banks recognize the partner relationship. | 1-3 business days |

| Offshore/Unregistered (e.g., Binance, KuCoin) | Not registered with FIU-IND; often blocked via ISP | High risk of rejection. Banks may flag the source as "unknown" or "high-risk". | Delayed or failed; requires manual verification |

| P2P Platforms | Peer-to-peer; no direct bank-exchange link | Very high scrutiny. Incoming payments from individuals look like personal transfers, not commercial sales. | Instant but risky if counterparty is flagged |

If you use a compliant exchange, the money comes into your bank account with clear metadata showing it came from a registered entity. This makes the bank's job easier. If you use an offshore exchange that hasn't registered with the FIU-IND, the payment gateway might route funds through third-party processors that lack transparency. To a bank manager, this looks opaque and dangerous. They are likely to ask for extensive documentation or reject the deposit entirely.

Documentation Required for Smooth Withdrawals

To avoid having your account frozen or your withdrawal rejected, you need to be prepared. Think of yourself as your own compliance officer. Before initiating a large withdrawal, gather the following documents:

- Source of Funds Declaration: A simple letter stating where the crypto was acquired (e.g., "Bought Bitcoin in January 2023 using savings").

- Transaction History: Export your trade history from the exchange. Highlight the specific transactions you are converting to fiat. This proves the money is yours and earned legitimately.

- Tax Payment Proof: This is critical. Show evidence that you have paid the 1% TDS and the 30% capital gains tax. If you haven't filed your returns yet, provide an estimate or a receipt from a Chartered Accountant confirming the liability.

- KYC Documents: Ensure your bank has your latest PAN card, Aadhaar card, and address proof. Mismatched names between your exchange account and bank account are a common reason for rejections.

If you proactively send these documents to your bank before they ask, you demonstrate transparency. Most banks will release the funds quickly once they see you are not hiding anything.

The Impact of FATF Travel Rule

In 2023, India implemented the Financial Action Task Force (FATF) Travel Rule with no minimum threshold. This regulation requires that every crypto transfer includes detailed sender and receiver information. While this primarily affects cross-border crypto moves, it impacts domestic withdrawals too.

When you withdraw fiat, the exchange must verify your identity beyond standard KYC. They must ensure that the person receiving the INR is the same person who owns the crypto wallet. If there is any discrepancy-for example, if you try to withdraw to a friend's bank account-the transaction will fail. Banks strictly enforce this "beneficial owner" rule. You cannot use crypto as a gift mechanism easily; the money must flow back to the original owner's verified bank account.

What Happens If Your Bank Freezes Your Account?

It happens more often than you think. If your bank flags your account due to crypto activity, they may temporarily freeze it pending investigation. Here is how to handle it:

First, stay calm. Do not close the account immediately. Second, contact your branch manager directly. Email is better than phone calls because you can attach documents. Explain that you are a legitimate investor complying with all tax laws. Provide the documentation listed above. Third, if the bank refuses to budge, you can file a complaint with the Banking Ombudsman. However, this is a last resort. Most issues are resolved at the branch level once the bank sees clear proof of tax compliance and legitimate source of funds.

Remember, the goal of the regulators is not to stop you from investing. It is to bring crypto into the formal economy. By being transparent, you align yourself with their goals, making your life much easier.

Future Outlook: SEBI Regulation and CBDC

Looking ahead, the landscape is shifting again. Parliament is considering legislation that would place cryptocurrencies under the primary control of the Securities and Exchange Board of India (SEBI). This could mean stricter listing requirements for exchanges and even tighter reporting for investors. Additionally, the RBI is pushing hard for the Central Bank Digital Currency (CBDC), known as the e-Rupee. Governor Sanjay Malhotra has stated that CBDC offers benefits without the systemic risks of private crypto.

While the e-Rupee is not a replacement for Bitcoin or Ethereum, its introduction signals that the government wants digital finance to remain within its controlled ecosystem. Banks will likely prioritize CBDC transactions over private crypto conversions in the future. For now, however, the path remains open, provided you stay compliant.

Is it illegal to withdraw crypto to fiat in India?

No, it is not illegal. Since the Supreme Court judgment in 2020, buying, selling, and holding cryptocurrency is legal. However, you must comply with tax laws, including paying 1% TDS and 30% capital gains tax, and use exchanges registered with the FIU-IND.

Can my bank block my crypto withdrawal?

Yes, your bank can block or delay the withdrawal if they suspect money laundering or tax evasion. This is more likely if you use non-compliant offshore exchanges or if you cannot provide proof of tax payments and source of funds.

Which exchanges are safe for Indian users?

Exchanges that are registered with the Financial Intelligence Unit (FIU-IND) and comply with PMLA regulations are safest. Examples include CoinDCX and WazirX. Offshore exchanges like Binance and KuCoin have faced blocks and higher scrutiny from banks.

Do I need to declare crypto income to the bank?

You do not need to declare it to the bank specifically, but you must declare it to the Income Tax Department. However, if your bank asks for source of funds, providing your tax return filings is the best way to prove legitimacy.

What is the FATF Travel Rule impact on withdrawals?

The FATF Travel Rule requires exchanges to share detailed sender and receiver information for all transactions. This ensures that crypto withdrawals only go to the verified account holder, preventing anonymous transfers and reducing fraud risks for banks.

15 Comments

the entire premise of this article is built on a fragile house of cards that the RBI is only too happy to kick over at the slightest provocation. you think compliance is enough? it never was. the banks are not acting out of caution they are acting out of pure malice towards anyone who tries to opt out of their controlled ecosystem. the supreme court ruling was a temporary reprieve not a permanent solution and everyone pretending otherwise is deluding themselves. the moment the political winds shift slightly these so called compliant exchanges will be treated like pariahs again. do not trust the metadata because the metadata can be altered by the very entities you are trying to avoid. the travel rule is just another layer of surveillance designed to make privacy impossible for the average user. if you are holding crypto in india you are already walking on thin ice and no amount of tax receipts will save you from arbitrary freezing. the system is rigged against individual sovereignty and this guide is just teaching you how to be a better slave to the banking cartel.

I appreciate the detailed breakdown here as it provides a clear perspective on the current regulatory landscape which is often quite confusing for many investors. It is important to remember that while the legal framework has evolved significantly since 2020 the practical application by financial institutions remains cautious due to strict anti-money laundering protocols. This caution is understandable given the global pressure on banks to prevent illicit finance flows and ensure that all transactions are fully transparent and verifiable. For those looking to navigate this space successfully maintaining impeccable records and ensuring full compliance with local tax obligations is absolutely essential. The distinction between compliant and non-compliant exchanges is particularly crucial as using registered platforms significantly reduces the risk of transaction delays or account freezes. It is also worth noting that the introduction of the FATF Travel Rule adds an additional layer of identity verification which further emphasizes the need for accurate KYC documentation across all platforms. By staying informed and proactive individuals can mitigate many of the risks associated with crypto-to-fiat conversions in India.

actually i think the whole idea of needing permission to move your own money is fundamentally flawed and absurd. why should a bank get to decide if my assets are legitimate based on some arbitrary algorithm? it feels like we are going backwards instead of forwards into a more free society. the government wants control and thats all this is about control. but people will always find ways around it because freedom is innate. maybe one day they will realize that trust should be placed in code not in corrupt bureaucrats.

Oh, look at you! Trying to navigate the bureaucratic maze of Indian banking regulations with such earnestness! It’s almost adorable how you think having your tax receipts ready will magically appease the gods of compliance! But let’s be real here; the system is designed to frustrate you! Every step you take is monitored, scrutinized, and potentially blocked! You might have all the paperwork in the world, but if the branch manager has a bad day, guess what? Your funds are frozen! So, keep your documents tidy, keep your head down, and pray to the RNG gods that your exchange stays on the good side of the FIU-IND! Good luck, you’ll need it!

Stay focused on the facts. Compliance is key. Keep records clean.

The notion that one can simply withdraw cryptocurrency without encountering significant friction is a rather naive perspective held by those unfamiliar with the intricate nuances of international financial regulation. The Reserve Bank of India’s skepticism is not merely a bureaucratic hurdle but a fundamental stance rooted in the preservation of monetary stability. Those who engage in such transactions must possess a sophisticated understanding of the Preventive Money Laundering Act and its implications. It is imperative to recognize that the financial institutions operate within a rigid framework where deviation from established norms is met with severe repercussions. Therefore, the emphasis on using fully compliant exchanges is not merely a suggestion but a necessity for any discerning investor who values the security of their capital above all else.

You really think you can just walk in there with your little crypto bags and expect them to hand over the rupees? Please. These bankers know exactly what you are doing and they hate it. They are waiting for you to slip up so they can freeze everything and laugh while you beg for your money back. It is a game of cat and mouse and you are the mouse. Stop pretending you are safe just because some lawyer said it was legal. Legal does not mean safe. It means they can arrest you later if they want to. Enjoy your prison cell.

i feel like this is super helpful info tho. its scary how much power banks have right? like why cant we just send money freely? but yeah i guess we gotta follow the rules or else. hope my coinDCX works fine next time i try to cash out. fingers crossed lol.

Let me tell you something that most people don't understand about this whole situation. The banks are not just following rules they are actively participating in a suppression campaign against decentralized finance. You see when they block these transactions they are sending a message that your wealth is not truly yours unless they say so. I have seen this happen time and time again with clients who thought they were safe. They were wrong. The only way to stay ahead is to diversify your exit strategies and never rely on a single bank or exchange. Always have a backup plan because the system is designed to fail you when you need it most. That is the reality of the modern financial world.

lol who reads this stuff anyway. just buy bitcoin and hold it forever then nobody can stop u. banks r useless anyway. why bother withdrawing? lets just live under rocks and eat bugs. easy fix.

Look man i get the frustration but you gotta play the game smart. dont fight the system directly. use the tools they give you. file your taxes show your proof. be boring. be predictable. that is how you win. if you act suspicious they will crush you. so just be a normal guy who happens to like crypto. its all about perception. change your vibe and they will leave you alone. trust me i have seen it work.

This is exactly why I believe that cryptocurrency is inherently immoral and dangerous. It encourages tax evasion and undermines the social contract that holds our society together. People who engage in these activities are selfish individuals who care only about their own gains at the expense of the community. The banks are right to be aggressive because they are protecting the integrity of the financial system. If you cannot provide clear and verifiable proof of your income then you deserve to have your accounts frozen. It is simple justice. We need stricter laws and harsher penalties for anyone who tries to bypass the traditional banking system.

Oh great another guide on how to please the masters. Look at you trying to be so compliant. Do you really think they care about your tax receipts? No. They care about power. And you are giving it away willingly. What a joke. You are basically begging them to let you keep your money. Pathetic. Just wait until they change the rules again and then you will cry. Spoiler alert: you will cry.

Brilliant piece of analysis! It really highlights the tension between innovation and regulation. While the restrictions are frustrating for users they are necessary for the long term health of the market. We must support compliant exchanges and encourage transparency. This is the only way we can build a sustainable future for digital assets in India. Let us keep pushing for clarity and fairness in the process!

i understand how stressful this must be for everyone involved. it is hard to feel secure when the rules seem to change so often. please take care of yourselves and stay calm during these times. knowing that you are doing everything right is important even if the system does not always reflect that. you are not alone in this struggle