Ecuador Banking Ban on Crypto Transactions: What It Means for Users and the Market

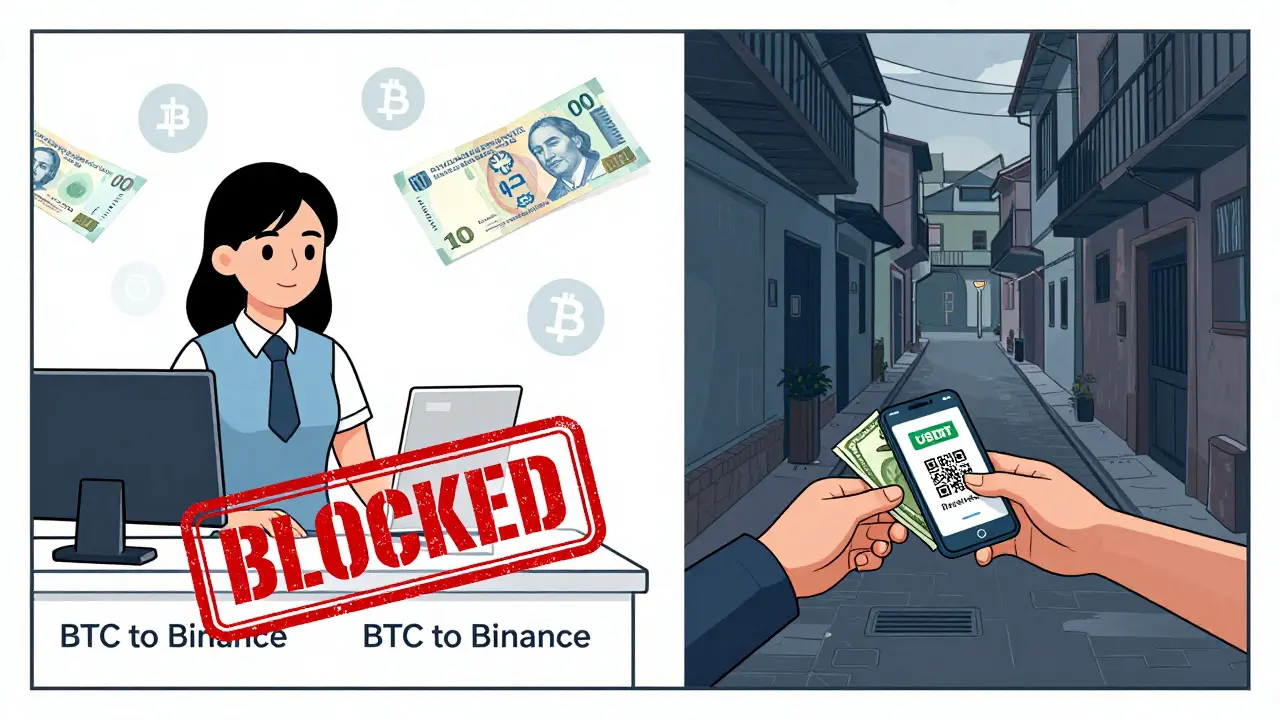

When Ecuador banned its banks from handling cryptocurrency transactions in 2022, it didn’t just make a policy change-it created a parallel financial system. Today, over 385,000 Ecuadorians still use crypto, but they can’t do it through their banks. No deposits. No withdrawals. No direct transfers. If you try to send money to Binance or OKX from your Banco Pichincha account, it gets blocked. Sometimes, your account gets frozen for weeks. And if you’re lucky, you’ll get a call from your bank asking why you sent $200 to a crypto exchange.

Why Ecuador Banned Crypto Through Banks

Ecuador dollarized its economy in 2000. That means the U.S. dollar is the only legal tender. No sucres. No bolivares. No pesos. Just dollars. The Central Bank of Ecuador (BCE) sees cryptocurrency as a threat to that system. Why? Because if people start using Bitcoin or Ethereum like money, it could weaken trust in the dollar. And in a country that relies on remittances, tourism, and imported goods, losing confidence in the dollar could mean economic chaos. In January 2022, the Junta de Política y Regulación Monetaria y Financiera (JPRM) issued Resolution 001-22. It didn’t say crypto was illegal. It said financial institutions could not process crypto transactions. That’s the key. The BCE can’t ban you from owning Bitcoin. But it can-and does-ban banks from touching it. By March 2023, Resolution 002-23 made it official: crypto is not a payment method. You can’t pay for groceries, rent, or a bus ticket with Bitcoin. You can’t even sign a contract in Ethereum. The law is clear: only dollars count.How the Ban Works in Practice

The Superintendency of Banks (SB) doesn’t just issue rules. It enforces them. Every bank in Ecuador must install a Transaction Monitoring System (TMS) Version 3.1 by January 1, 2025. This system flags 47 specific crypto-related patterns:- Transfers to known exchange addresses (Binance, OKX, Mercado Bitcoin)

- Multiple small deposits under $200 to avoid detection

- Transactions with wallets linked to Telegram-based OTC desks

- Payments labeled as "gift cards" or "online services" that match crypto purchase patterns

What People Do Instead

You can’t use your bank, but you can still buy crypto. You just have to get creative. Most Ecuadorians use peer-to-peer (P2P) trading. They meet sellers in person, pay in cash, and get Bitcoin sent to their wallet. Or they use Telegram groups. There are dozens of active P2P groups where users trade USDT (Tether) for cash. The average transaction size? $1,250. That’s not pocket change. That’s rent, school fees, medical bills. Some use gift cards. Buy a $500 Amazon gift card with crypto. Sell it in person for cash. Others use prepaid dollar cards issued by non-bank companies-like those from Payoneer or Wise-that don’t ask where the money came from. These work, but they cost 4.8% in fees on average. In Colombia, where crypto is legal, fees are 1.2%. And then there’s the stablecoin workaround. Many users convert crypto to USDT first. Then they try to send USDT as a regular USD transfer. Sometimes it goes through. Sometimes it doesn’t. In Q2 2025 alone, 147 users reported frozen funds totaling $382,000 because their bank flagged the transaction as suspicious.

Who’s Affected the Most

It’s not just crypto traders. It’s remittance senders. Ecuador gets billions in dollars from family members abroad. Traditional remittance services charge 6.5% on average. Crypto could cut that to under 1%. But banks won’t let it happen. A 2024 study by Pontificia Universidad Católica del Ecuador found that 78% of crypto users convert crypto to cash through informal channels. Why? Because 61% said they had no other way to access money. That’s not a choice. That’s necessity. The unbanked are hit hardest. Over 42% of Ecuadorian adults don’t have a bank account. For them, crypto was supposed to be a lifeline. Now, it’s a dead end. They can’t use apps like PayPal or Wise because those services are tied to the banking system. And without a bank, they can’t cash out.The Legal Gray Zone

Here’s the twist: owning crypto isn’t illegal. Trading it privately isn’t illegal. Mining it isn’t illegal. In fact, there are over 1,000 mining operations in Ecuador now-up from just 100 in 2023. But none of them have bank accounts. They pay their electricity bills in cash. They buy equipment through intermediaries. They pay taxes on profits using cash receipts. The Internal Revenue Service (SRI) taxes crypto gains at up to 35% for individuals. That’s higher than the U.S. rate. But enforcement is weak. Most people don’t report. Why? Because reporting means leaving a trail. And if you leave a trail, the bank might notice. There’s also Bill 6538, introduced in May 2025 by Congresswoman Shirley Rivera. It proposes licensing crypto exchanges with $500,000 minimum capital, proof-of-reserves audits, and real-time monitoring. But it’s stuck in three congressional committees. Analysts say it won’t pass before 2027.

What’s Next?

The Central Bank is testing a digital currency-the BCE’s own CBDC. It’s expected to launch in late 2025. If it’s designed to replace private crypto, it could make things worse. If it’s designed to coexist, it might open the door for reform. Right now, Ecuador is caught between two worlds. One where the dollar rules everything. One where technology moves faster than law. The result? A system that punishes innovation, isolates the unbanked, and pushes people into risky, expensive workarounds. For now, the ban stands. Banks still block. Users still trade. And the gap between what the law says and what people do keeps growing.FAQ

Can I legally own Bitcoin in Ecuador?

Yes. Owning, buying, or selling Bitcoin privately is not illegal in Ecuador. The ban only applies to banks and financial institutions. You can hold crypto in a wallet, trade on P2P platforms, or mine it. But you can’t use a bank account to deposit, withdraw, or transfer crypto-related funds.

What happens if my bank freezes my account for crypto activity?

Your account will be frozen for 3 to 14 days on a first offense. The bank will ask for proof that the transaction wasn’t for crypto. If you can’t prove it, they may close your account. Many users report being asked to sign statements saying they won’t use crypto again. Refusing can lead to permanent closure. There’s no formal appeal process.

Can I use USDT (Tether) to bypass the ban?

Some users try. They convert crypto to USDT, then send it as a "regular USD transfer"-labeling it as a gift, payment for services, or online purchase. Occasionally, it works. But banks now flag USDT transfers with the same systems used for Bitcoin. In Q2 2025, $382,000 in frozen funds came from USDT attempts. It’s risky. You could lose money with no recourse.

Do I have to pay taxes on crypto gains in Ecuador?

Yes. The Internal Revenue Service (SRI) taxes crypto profits at up to 35% for individuals and 25% for businesses. But enforcement is minimal. Most users don’t report because reporting creates a paper trail that could trigger bank scrutiny. The SRI doesn’t actively track wallets, but if you deposit crypto profits into a bank account, they may notice.

Is there a chance the ban will be lifted soon?

Unlikely before 2027. Bill 6538 proposes a licensing system, but it’s stuck in committee. The Central Bank continues to warn against crypto, and the government remains focused on protecting dollarization. Meanwhile, the CBDC pilot launches in late 2025. If it’s designed to replace private crypto, the ban will likely stay. If it’s designed to coexist, pressure for change may grow-but not fast.

Why don’t more people just move to a country with crypto-friendly banks?

Many do. But for most Ecuadorians, leaving isn’t an option. Remittances, family ties, jobs, and cost of living keep people in the country. The crypto ban isn’t just a policy-it’s a barrier to financial freedom for millions who can’t afford to relocate. The workaround isn’t freedom. It’s survival.

15 Comments

Man, I just read this and I’m honestly impressed by how resilient people are. Even with banks blocking everything, Ecuadorians are still finding ways to survive using crypto. P2P trades, Telegram groups, gift cards-it’s wild but also kind of beautiful. People aren’t giving up. They’re adapting. That’s the spirit of innovation right there.

And let’s be real: if you’re sending remittances and saving 5.5% on fees, why shouldn’t you? The system’s broken, not the people trying to use it. Kudos to everyone keeping this alive.

It’s not about rebellion. It’s about dignity. You deserve access to your own money.

I hope the CBDC doesn’t just replace crypto with another gatekeeper. Maybe it can open doors instead of slamming them shut.

This is what happens when you let unregulated assets infiltrate a dollarized economy. The ban isn’t oppressive-it’s necessary. Banks aren’t the villains; they’re following the law. People who ignore it are gambling with their financial stability.

I’ve been following this for a while. The fact that 1,000 mining operations exist without bank accounts is insane. Imagine running a business and paying electricity bills in cash. That’s not a workaround-that’s a full-on underground economy. And honestly? It’s working. People are getting by. The system’s not failing. It’s just evolving outside the rules.

The real tragedy isn’t the ban-it’s that people are being forced into risky P2P trades just to pay rent. If the government cared, they’d fix the system instead of punishing the most vulnerable. This isn’t about crypto. It’s about class. The rich can move money. The poor have to risk their lives doing cash meetups. That’s not freedom. That’s exploitation.

You know what’s ironic? The same people who scream about financial sovereignty are now using crypto like a magic wand. It’s not a currency. It’s a speculative asset. And yet, here we are-Ecuadorians treating USDT like cash, pretending it’s not volatile, pretending it’s not risky. The dream of decentralization is beautiful. The reality? It’s a barter economy with extra steps. 🤷♂️

The Central Bank of Ecuador has one mandate: preserve dollarization. Every transaction flagged, every account frozen, every fine issued-it is not punishment. It is preservation. To allow crypto into the financial system is to invite hyperinflation by proxy. The people using P2P are not heroes. They are vectors of systemic risk. The state is not cruel. It is prudent.

I’ve read a lot about this. The part about USDT being flagged as suspicious makes sense. Banks use pattern detection, not intent. If you send $199 three times in a row to the same address, it looks like smurfing. Doesn’t matter if you’re paying rent. The system sees risk, not reason. It’s flawed but not malicious. Just outdated.

Everyone’s acting like this is a crisis. Newsflash: crypto was never meant to be a banking solution. It was meant to be a hedge. Ecuadorians aren’t using Bitcoin to pay for groceries-they’re using it to preserve value. And guess what? That’s working. The fact that they’re getting fined and frozen out just proves how threatened the system is. They’re not breaking the law. They’re exposing its fragility.

I find it fascinating how a country that adopted the dollar to stabilize itself is now creating a parallel economy because its institutions refuse to adapt. This isn’t a crypto story. It’s a story about bureaucracy. The BCE isn’t protecting the dollar. It’s protecting its own relevance. And the people? They’re just trying to live in a world that no longer works for them.

The real issue here is not crypto but the lack of financial innovation in Ecuador. If banks had offered low cost remittance services people would not need to use P2P. The ban is a symptom not the cause. The system failed to serve the people so the people built their own. That’s not illegal. That’s human.

I don’t care how many people are using crypto. This is a mess. People are getting their accounts frozen. They’re losing money. They’re risking their safety meeting strangers for cash. This isn’t freedom. It’s chaos. And someone needs to fix it before someone gets hurt.

What’s being ignored is that this ban disproportionately affects the unbanked. Over 42% of adults don’t have accounts. Crypto was their only path to inclusion. Now they’re stuck between a rigid state and predatory informal markets. The real crime isn’t using Bitcoin-it’s failing to create alternatives. Policy should empower, not exclude.

I’ve been reading this thread. The part about miners paying electricity in cash stuck with me. That’s not a loophole. That’s a revolution. People aren’t just trading crypto. They’re rebuilding economic relationships outside the system. No banks. No intermediaries. Just trust and cash. It’s messy. It’s dangerous. But it’s real.

This whole thing is a psyop. The CBDC is coming. They’re using crypto as an excuse to push a government-controlled digital dollar. They want to track every transaction. They want to freeze your account if you buy a Tesla. They already know who you are. This ban? It’s not about stability. It’s about control. 🤖💸

Let me break this down logically because clearly no one else is. The dollarization policy was designed to prevent inflation. Crypto introduces volatility. Volatility undermines confidence. Confidence is the foundation of a dollarized economy. Therefore, crypto must be restricted. This is not censorship. It is macroeconomic hygiene. The fact that people are still trading is proof that the system is under stress. The solution is not to legalize crypto. The solution is to strengthen the dollar’s institutional backing. Which means more regulation, not less. And yes, I know this makes life harder for people. But economics is not a popularity contest. It is science. And science does not care about your feelings.