Crypto as Property: US Tax Treatment for Bitcoin

When you buy, sell, or spend Bitcoin in the United States, you're not just making a digital transaction-you're triggering a taxable event. The IRS doesn't treat Bitcoin as money. It treats it as property. That single classification changes everything about how you report gains, track losses, and plan your finances. Whether you bought Bitcoin in 2017, mined it last year, or used it to pay for groceries in 2026, the IRS sees each move as a sale of an asset. And that means you owe taxes on every profit, no matter how small.

Why Bitcoin Isn't Treated as Currency

The IRS made this clear back in 2014 with Notice 2014-21. At the time, Bitcoin was still a niche experiment. But the agency didn’t wait for public opinion or market trends. It looked at the legal definition of currency and saw that Bitcoin lacked key features: it’s not issued by a government, it’s not legal tender, and it doesn’t have a fixed value tied to a national economy. So instead of treating it like dollars or euros, the IRS classified it as property-just like stocks, real estate, or gold. This isn’t just bureaucracy. It has real consequences. If you use Bitcoin to buy a laptop, you’re not just trading digital tokens. You’re selling an asset. If the Bitcoin you spent was worth $800 when you bought it and $1,200 when you used it, you just made a $400 capital gain. That gain is taxable. No exception. No threshold. Not even for small purchases.Three Ways Bitcoin Can Be Classified (And What It Means for Your Taxes)

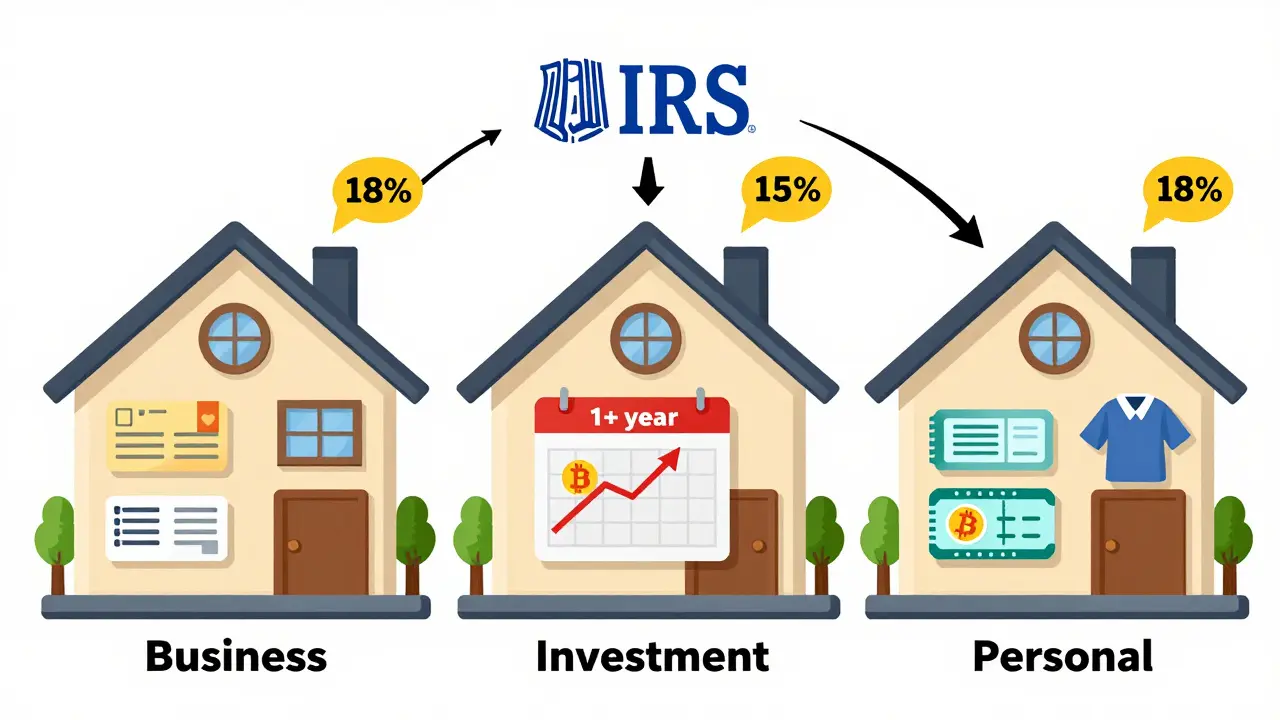

Not all Bitcoin is taxed the same. The IRS recognizes three main categories, each with different rules:- Business Property: If you mine Bitcoin as part of a business-say, you run a mining rig and sell the output-then your Bitcoin is treated like inventory. Any profit from selling it is taxed as ordinary income, at your regular income tax rate, which can go as high as 37%. You can deduct expenses like electricity, hardware, and software, but you must keep detailed records of costs and sales.

- Investment Property: This is the most common category. If you bought Bitcoin hoping it would go up in value and you hold it for more than a year before selling, you qualify for long-term capital gains rates. For 2024, those rates are 0%, 15%, or 20%, depending on your income. Single filers pay 0% if their taxable income is under $47,025. Married couples filing jointly pay 0% if under $94,050. That’s a huge advantage over short-term gains, which are taxed as ordinary income.

- Personal Property: This applies when you use Bitcoin to buy things for personal use-like paying for a vacation, buying clothes, or tipping a streamer. Even though it’s personal, the IRS still treats it as a sale. If you bought 0.1 BTC for $3,000 and later used it to pay for a $4,500 trip, you’ve realized a $1,500 gain. That’s taxable. No personal exemption exists here.

How to Calculate Your Gain or Loss

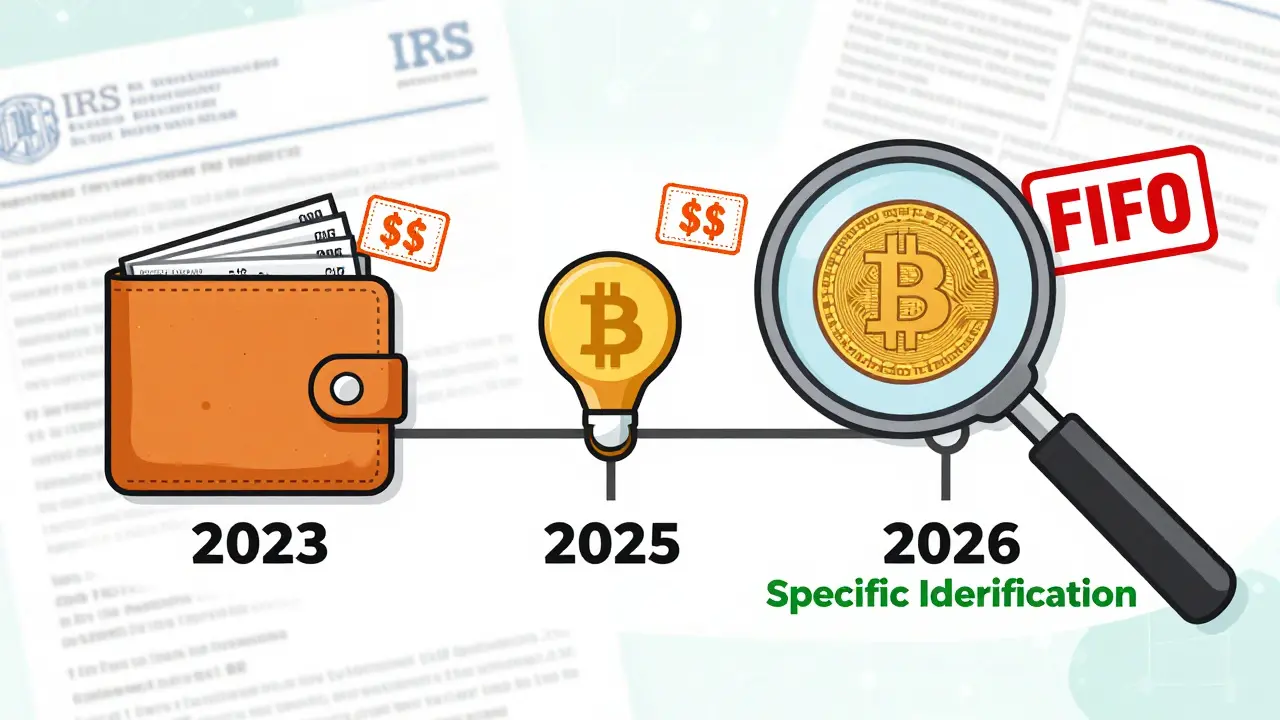

The math isn’t complicated, but the record-keeping is. Every time you buy Bitcoin, you establish a cost basis-the amount you paid for it, including fees. Every time you sell, trade, or spend it, you calculate the difference between that basis and what you received. For example:- You bought 1 BTC on March 10, 2023, for $30,000.

- You bought another 1 BTC on August 5, 2023, for $35,000.

- You sold 1.5 BTC on February 12, 2026, for $75,000.

Hard Forks and Airdrops: Unexpected Tax Triggers

Crypto isn’t just about buying and selling. Sometimes, a blockchain splits. Bitcoin Cash emerged from Bitcoin in 2017. Ethereum Classic from Ethereum. These are called hard forks. And if you receive new coins from one, the IRS says: welcome to taxable income. If a hard fork happens and you don’t get any new coins? No tax. Simple. But if you get an airdrop-new coins automatically deposited into your wallet-you owe taxes on the fair market value of those coins the moment you can control them. Say you received 5 ETH from an airdrop on January 15, 2025, and it was worth $3,200 that day. You owe ordinary income tax on $3,200. Your basis in those ETH? Also $3,200. That becomes your new starting point for future sales. The IRS defines “control” as having the private keys and being able to transfer, sell, or trade the asset. If the coins are stuck in a wallet you can’t access? No tax until you can move them.What You Must Track (And How to Do It)

The IRS doesn’t care if you’re a casual holder or a full-time trader. You need records for every transaction:- Date and time of each purchase

- Amount paid (in USD) and fees

- Source (exchange, peer-to-peer, mining)

- Wallet address used

- Date and time of each sale, trade, or spend

- Value received (in USD) at the time of transaction

- Purpose of the transaction (investment, personal use, business)

Why the GENIUS Act and CLARITY Bill Didn’t Change Anything

In July 2025, Congress passed the GENIUS Act, which created clearer rules for crypto exchanges, stablecoins, and reporting. Later, the House passed the CLARITY Bill, which proposed a $600 threshold for reporting crypto transactions-similar to how banks report cash deposits. But here’s the catch: neither law changed the core tax treatment. The IRS still says: Bitcoin is property. Not currency. Not a security. Not a commodity. Property. Even when the SEC says a token is a security, the IRS doesn’t follow suit. One agency regulates markets. The other collects taxes. They operate under different laws. So if you hold a token the SEC calls a security, you still pay capital gains tax on it, not income tax. The IRS doesn’t care about regulatory labels. It cares about how you use the asset.What Happens If You Don’t Report

The IRS added a simple question to Form 1040 in 2020: “At any time during 2024, did you receive, sell, send, exchange, or otherwise acquire any financial interest in any virtual currency?” Answering “No” when you should’ve said “Yes” is fraud. The IRS has been auditing crypto users since 2021. They get data from exchanges like Coinbase, Kraken, and Binance US. They match transaction records with tax returns. If you sold $10,000 worth of Bitcoin and didn’t report it? You’ll get a notice. Penalties start at 20% of the underpaid tax. If they think you’re hiding it intentionally? That’s 75%. Plus interest. There’s no statute of limitations on fraud. The IRS can go back 10 years if they suspect intentional evasion.What’s Next?

There’s no sign the IRS is changing its stance. Even as crypto adoption grows-over 46 million Americans now own digital assets-the tax rules remain stubbornly clear. Property. Every transaction. Every gain. Every loss. The complexity isn’t going away. But the tools are getting better. More exchanges now auto-generate tax reports. More accountants specialize in crypto. More people are using software to track their holdings. The bottom line: If you own Bitcoin in the U.S., you’re a property owner. And property owners pay taxes on what they sell. There’s no loophole. No exemption. No magic number. Just rules-and consequences.Do I owe taxes if I only bought Bitcoin and never sold it?

No. Buying Bitcoin with cash or transferring it between your own wallets isn’t a taxable event. Taxes only apply when you sell, trade, spend, or receive Bitcoin as income. Holding alone doesn’t trigger taxes.

What if I trade Bitcoin for Ethereum? Is that taxable?

Yes. Trading one cryptocurrency for another is treated as two separate events: selling your Bitcoin for USD, then buying Ethereum with that USD. You must calculate the gain or loss on the Bitcoin sale. There’s no like-kind exchange (1031) loophole for crypto anymore-those ended after 2017.

Can I use the FIFO method if I don’t track my transactions?

Yes. If you can’t prove which Bitcoin units you sold, the IRS assumes you sold the oldest ones first (FIFO). This might result in higher taxes if your earliest purchases were cheaper. Using specific identification with proper records can save you money.

Do I have to report Bitcoin received as payment for work?

Yes. If you’re paid in Bitcoin for services, it’s taxable income at the fair market value on the day you received it. Your employer should issue a Form 1099-NEC if you’re an independent contractor. You’ll also need to track your basis for future sales.

What if I lost access to my wallet? Do I still owe taxes?

You still owe taxes on any gains you realized before losing access. If you sold Bitcoin and then lost the wallet, the tax liability remains. Losses from lost or stolen crypto are generally not deductible under current tax law, unless tied to a federally declared disaster.