Can Businesses in Nigeria Accept Crypto Legally? The 2026 Rules

Is It Legal to Take Crypto as Payment in Nigeria?

If you run a business in Nigeria and want to accept Bitcoin or USDT directly from customers, the short answer is no. Not exactly.

The rules changed dramatically in March 2025 with the signing of the Investments and Securities Act (ISA) 2025, which defines digital assets as securities regulated by the Securities and Exchange Commission (SEC). This law killed the old gray area where businesses could just set up a wallet and start taking payments. Now, unless you are a licensed financial entity, accepting crypto for goods or services is technically illegal.

This creates a confusing situation. Nigerians love crypto. According to Chainalysis data from early 2025, about 32% of the population uses it. But the government treats it like a stock, not cash. So, while your customer can legally own Bitcoin, they cannot legally hand it to you at the checkout counter unless you have a specific license. If you try to do it anyway, you risk warnings from the SEC or worse.

Why Direct Payments Are Banned

To understand why you can't just accept crypto, you have to look at how the Central Bank of Nigeria (CBN) views money. Under the CBN Act of 2007, only the Naira is legal tender. The ISA 2025 reinforced this. Digital assets are classified as investment instruments, similar to shares or bonds.

Think of it this way: if someone wants to pay you for a laptop using shares in a company, you don't just take the paper certificate and call it a day. You usually need a broker to convert those shares into cash. The Nigerian government wants the same process for crypto. They want to prevent money laundering and protect investors, so they force all transactions through regulated channels.

In 2021, the CBN banned banks from servicing crypto exchanges entirely. That forced everyone to use peer-to-peer (P2P) methods, which were messy and risky for businesses. The ISA 2025 fixed the banking ban but added strict licensing requirements. Banks can now work with crypto firms, but only if those firms are approved by the SEC.

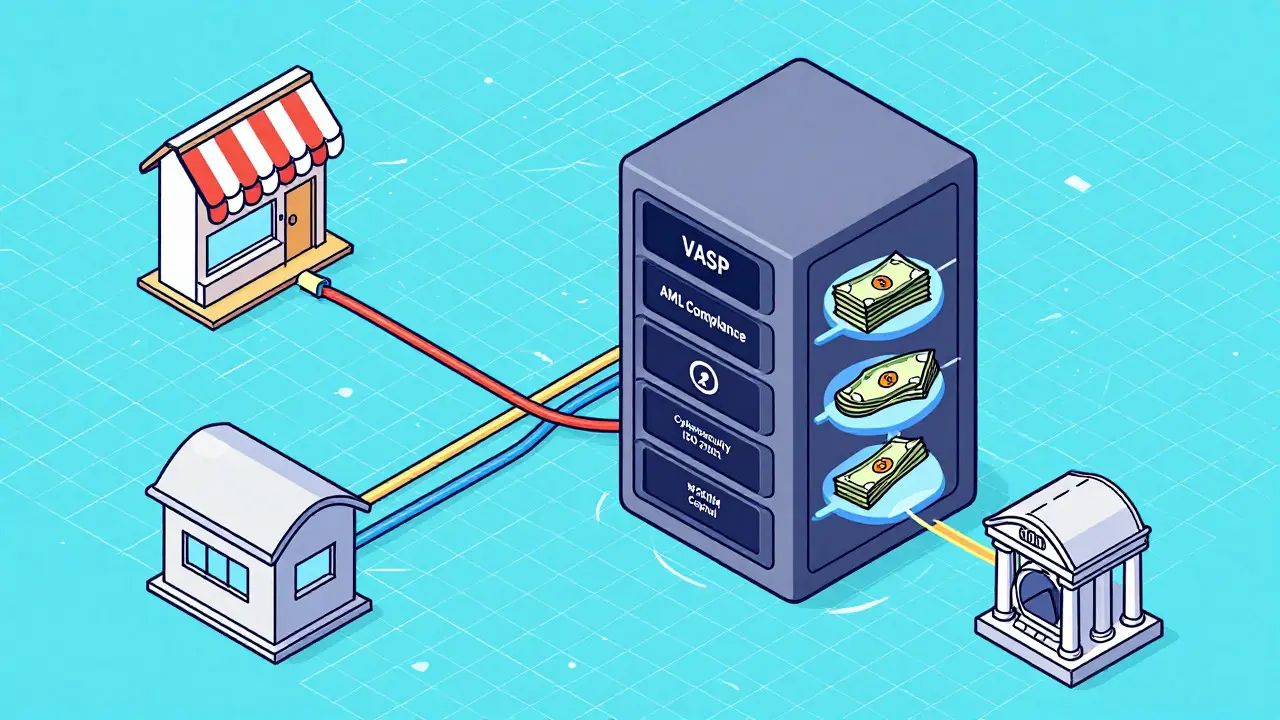

The Only Legal Way: Becoming a VASP

So, how do you legally touch crypto in your business? You must become a Virtual Asset Service Provider (VASP), also known as a Digital Asset Operator (DOP) or Digital Asset Exchange (DAE). These are entities authorized by the SEC to handle digital assets.

Getting this license is not easy. It is designed for serious financial institutions, not small shops. Here is what the SEC requires:

- Minimum Capital: You need at least ₦500 million (about $350,000 USD) in paid-up capital. This alone shuts out most small and medium-sized enterprises.

- AML/CFT Compliance: You must have robust Anti-Money Laundering and Combating the Financing of Terrorism systems. This means tracking every transaction and reporting suspicious activity to the Nigerian Financial Intelligence Unit (NFIU).

- Cybersecurity Standards: Your systems must meet ISO/IEC 27001 standards. You need 24/7 monitoring and cold storage solutions for 95% of client assets.

- Documentation: The SEC asks for 27 distinct documents, including proof of office space, executive background checks, and detailed operational manuals.

The application process takes an average of 145 days, and the initial rejection rate is 63%. Most rejections happen because applicants lack proper AML procedures or enough capital. For a typical retailer, restaurant owner, or online seller, this path is effectively closed.

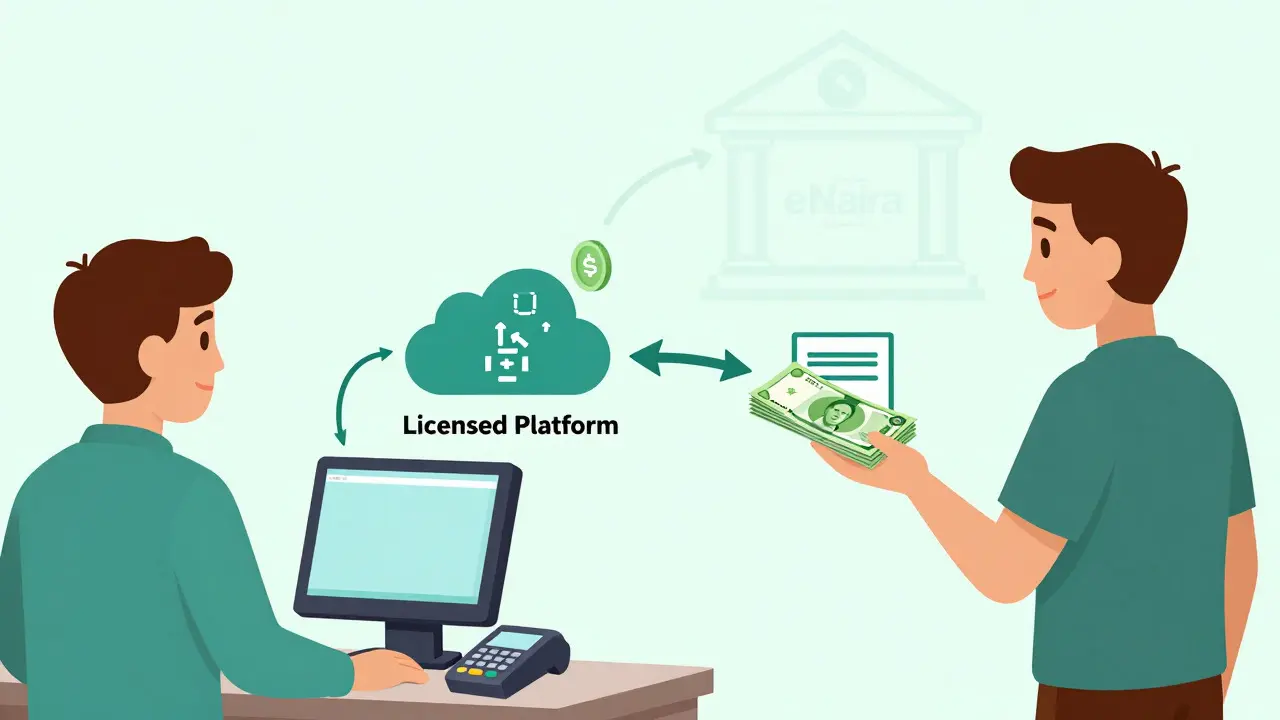

The Practical Solution: Partnering with Licensed Platforms

Since becoming a VASP is too expensive and complex for most, the standard workaround is to partner with one. Companies like Quidax, a leading Nigerian crypto exchange with significant market share, Bybit Nigeria, and Binance Nigeria are all SEC-licensed VASPs.

Here is how it works in practice:

- Your customer pays you in crypto via the platform’s payment gateway.

- The platform instantly converts the crypto into Naira.

- The Naira is deposited into your bank account.

You never actually hold the crypto. From a legal standpoint, the VASP handled the digital asset transaction, and you received fiat currency. This keeps you compliant with the ISA 2025.

However, there are costs. These platforms charge fees ranging from 1.5% to 3.5% per transaction. On top of that, you still have to deal with normal banking charges. For high-volume businesses, these fees eat into margins. For small sellers, it might make crypto payments unprofitable compared to traditional transfers.

| Method | Legal Status | Cost | Best For |

|---|---|---|---|

| Direct Wallet Transfer | Illegal for non-VASPs | Low (network fees only) | None (high risk) |

| Becoming a VASP | Fully Legal | Very High (₦500M+ capital) | Large Fintechs/Banks |

| Partnering with VASP (e.g., Quidax) | Legal | Moderate (1.5-3.5% fee) | SMEs, E-commerce, Retail |

Real-World Impact on Merchants

Data shows that this regulatory shift has cooled merchant enthusiasm. A survey by Breet.io in July 2025 found that while 78% of Nigerian merchants tried to accept crypto before the ISA 2025, only 11% continued afterward. Why? Because the new rules made it harder.

One e-commerce store owner shared his experience on Reddit in September 2025. He used to accept Bitcoin directly until he got a warning letter from the SEC in January 2025. He had to shut down direct payments and switch to a licensed VASP. He noted that the 3.5% conversion fee plus compliance costs significantly reduced his profit margins.

Another vendor on Jumia complained about losing international customers who wanted to pay in USDT. Because he couldn't accept it directly, he had to guide them through a third-party platform, adding steps and friction to the checkout process. Many customers dropped off during that extra hassle.

Despite this, some large players are adapting. Multinational corporations like MTN and Airtel accept crypto through approved channels for international settlements. They have the resources to navigate the complexity. For smaller businesses, the barrier remains high.

How Nigeria Compares to Neighbors

Nigeria’s approach is stricter than some neighbors but more structured than others. Let’s look at the region:

- South Africa: More permissive. Businesses can accept crypto as payment under the Financial Sector Regulation Act. There is less red tape for merchants.

- Kenya: Very restrictive. Kenya completely prohibits cryptocurrency as payment for goods and services.

- Ghana: Moderate. Ghana’s 2023 Digital Asset Bill allows limited acceptance through a regulatory sandbox overseen by the Bank of Ghana.

An analysis by the African Fintech Network in June 2025 scored Nigeria’s framework at 7.2/10 for investor protection but only 4.8/10 for merchant adoption. The report criticized the securities classification for creating unnecessary complexity. Instead of treating crypto as a payment tool, Nigeria treats it as an investment product, which forces merchants into capital markets regulations rather than simple payment system frameworks.

What Comes Next? Regulatory Changes in 2026

The current system is under review. In September 2025, the SEC announced a six-month review of the merchant acceptance framework. Director General Emomotimi Agama acknowledged the need to balance innovation with stability.

Proposed amendments include creating a new category called "Digital Payment Vehicle." This would allow businesses to accept crypto with lower barriers:

- Lower Capital Requirement: Potentially dropping from ₦500 million to ₦50 million.

- Simplified Compliance: Streamlined AML procedures tailored for retail payments rather than investment trading.

Analysts at Fitch Ratings project that Nigeria will keep the securities classification through 2026 but may introduce these limited merchant pathways by Q2 2027. Meanwhile, the Central Bank of Nigeria launched the commercial phase of the eNaira, Nigeria's Central Bank Digital Currency (CBDC), in October 2025. With 1.2 million users in the first week, the eNaira offers a government-backed alternative for digital payments, potentially reducing pressure to liberalize private crypto payments.

Checklist for Businesses Wanting to Accept Crypto

If you are still determined to accept crypto in Nigeria today, follow this checklist to stay legal:

- Do NOT open a personal wallet for business payments. This violates the ISA 2025 if you are not a VASP.

- Choose a licensed VASP partner. Look for companies listed on the SEC’s registry of approved Virtual Asset Service Providers.

- Calculate the true cost. Add the VASP fee (1.5-3.5%) to your pricing model. Ensure your profit margin can absorb this.

- Inform your customers. Make it clear that they will be paying via a third-party platform that converts to Naira.

- Monitor regulatory updates. Follow the SEC and CBN announcements closely, especially regarding the proposed "Digital Payment Vehicle" category in 2026.

Can I accept Bitcoin directly into my wallet in Nigeria?

No, unless you are a licensed Virtual Asset Service Provider (VASP). The Investments and Securities Act (ISA) 2025 classifies crypto as securities, not currency. Direct acceptance by unlicensed businesses is illegal and risks SEC penalties.

What is the minimum capital to become a VASP in Nigeria?

The minimum capital requirement is ₦500 million (approximately $350,000 USD). This high barrier is designed to ensure only financially stable entities handle digital assets, protecting consumers from fraud.

Which platforms are legal for accepting crypto payments?

You must use SEC-licensed VASPs such as Quidax, Bybit Nigeria, or Binance Nigeria. These platforms act as intermediaries, converting crypto to Naira before depositing funds into your bank account, ensuring compliance with local laws.

Will the rules change in 2026?

Yes, potentially. The SEC is reviewing the framework and may introduce a "Digital Payment Vehicle" category with lower capital requirements (around ₦50 million) by 2027. Keep an eye on official SEC announcements for updates.

Is the eNaira a better alternative for businesses?

For domestic transactions, yes. The eNaira is legal tender backed by the Central Bank of Nigeria, meaning no conversion fees or regulatory hurdles. However, it lacks the global interoperability of cryptocurrencies like Bitcoin or USDT for international clients.